15.01.25 - Action-packed day - inflation concerns fade

Wednesday, a day packed with crucial economic data and the kickoff of earnings season.

UK: inflation lower than expected. Inflation rate 2.5% YoY vs. 2.6% consensus estimate.

Germany: economy continues to shrink, as expected, for second year in a row. German GDP -0.2% YoY (2024) vs. -0.3% YoY (2023).

US: inflation data inline: CPI 0.4% MoM and 2.9% YoY, both as expected.

Corporate earnings: reporting season started with US banks. JPMorgan, Goldman Sachs, BlackRock, WellsFargo, Citigroup, all banks reported sales and earnings above estimates.

Markets: Inflation prints are taken positive for risk assets.

UK: interest rates decline based on latest inflation figures, pound rises following recent slump through market turmoil.

Germany/Europe: Stock indices rise with some regained confidence.

US: Stock Futures jump after inflation report and strong bank earnings, US yields and US dollar decline.

Sentiment: No sharp reaction, only little move from “extreme fear” to fear level.

My View: As I mentioned few days ago, I did not share the common view that inflation would skyrocket. Therefore, today’s release is not much of a surprise to me.

I am happy with the latest tactical calls mirroring this view: buying US longterm Treasuries (leveraged ETF, 07.01.25), longterm UK Gilts (leveraged ETF, 14.01.25), hedging the US dollar (14.01.25), buying some pounds (14.01.25), adding long volatility (leveraged ETF, 16.12.24) and shorten the semiconductor sector (leveraged ETF, 07.01.25).

I continue to believe that interest rates will stabilize and show a tendency to decline, returning to levels observed a few weeks and months ago.

It is fair to say that increasing equity exposure as a tactical move could also be considered an investment opportunity. However, given my current equity allocation and significant volatility currently affecting equities, I opted not to add more risk to this asset class. Additionally, I am not yet convinced that today’s equity rally will prove to be sustainable.

Become a member to access more valuable market updates like this.

14.01.25 - Attempt to rebound after inflation reading

The producer price index (PPI) rose 0.2% in December, less than the 0.4% increase in November and below the consensus estimate for 0.3%. Producer prices are a leading indicator of consumer prices. The release is the first of two key inflation readings published this week.

Markets: Markets and risk assets seem to stabilize since the latter part of yesterday’s trading session. Asian indices showed a strong rebound, European and US markets try to follow however rather shy. Interest rates are moving sideways.

My View: Markets are attempting to stabilize, but in my view, the rebound appears too modest following the recent drop in stock prices. Before increasing my equity exposure - whether by closing my short positions or buying additional stocks - I want to see a more decisive upward movement and a clearer indication of investor confidence.

As investors seem to overreact on the inflation topic, I expect interest rates to normalize and return to lower levels on some point. At the same time, the US dollar could lose some ground following its recent rally. I have started hedging a portion of my USD exposure against the Swiss franc at the price of 0.91702.

As the same story is cooked in the UK, I decided to gain some exposure to longterm UK Gilts (UK government bonds) to my portfolio today, implementing this strategy through an ETF.

Become a member to access more valuable market updates like this.

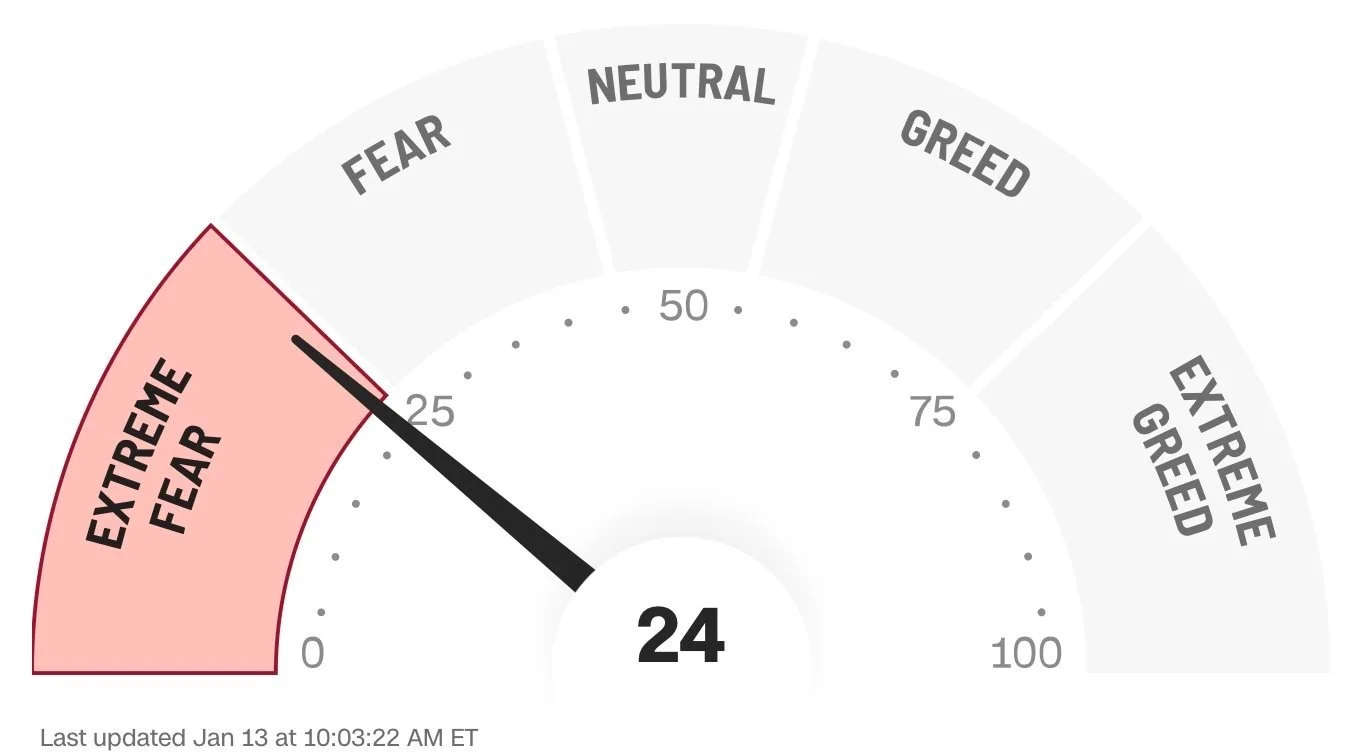

13.01.25 - Extreme fear hits markets

The CNN Fear & Greed Index hits the “Extreme Fear” level, indicating the risk aversion among investors. The index is a measure of market sentiment, based on factors such as volatility, stock price momentum, market breadth, and demand for safe assets like bonds.

Markets: Market sell-off continues on a broad base as interest rates and volatility rise.

My View: Cross-asset correlation starts to increase indicating a heightened market uncertainty and the broader market correction. Investors got caught on the wrong foot starting the investment year 2025 with pure optimism around. In December, the cash levels hit the lowest level. All-in stance without any hedging as the put/call ratio is still on low levels.

The Fear & Greed Index is a contrarian indicator. A “extreme fear” level normally indicates a buying opportunity. However, as the momentum of increasing interest rates might continue, further downward pressure on equities cannot be ruled out in the short-term. Markets seem to be close to some support levels. Before I go back to increase my risk exposure, I would like to see these technical support levels to be successfully tested.

Based on the latest market patterns, the pendulum could easily hit the downside as an overreaction could be seen for once also on the negative side. A negative momentum is just about to start and the speculative traders did not yet leave the market.

Become a member to access more valuable market updates like this.

13.01.25 - China surprises

China’s exports surged in December by 10.7% from a year earlier, higher than the expected 7.3%, while imports were up 1% (expected -1.5%). Ahead of Donald Trump’s return to the White House, China’s trade surplus hits a record high.

Markets: Chinese indices managed to recover some of the losses after the release, but ended the session in the red. Downward pressure in equity markets across the globe amid rising U.S. interest rates and risk aversion.

My View: somehow the upbeat in exports does only surprise on first sight. It seems companies rushed to deliver goods out of the country before Donald Trump returns to the White House. More evidence about China’s economy with data on GDP growth, retail sales, or industrial production will follow on coming Friday. This has room to sway market sentiment. I remain optimistic that Chinese stocks have an upside potential, favoring the internet sector, implemented via an ETF.

Become a member to access more valuable market updates like this.

12.01.25 - Key week ahead

During the coming week, an important set of economic data will be released, alongside the kickoff of earnings season. Wednesday could become a hot day. The big banks like JPMorgan, Citigroup, BlackRock, Goldman Sachs and Wells Fargo are set to report their fourth quarter results. On the same day, new inflation data will be released.

Already on Monday morning, investors will closely watching economic data out of China, including the latest import/export figures followed by a substantial data release on Friday, featuring GDP growth and other critical indicators.

Markets: - (only cryptos are trading over the weekend, sideways in a wide range)

My View: a crucial week for financial markets could be ahead of us. After the hot job report on Friday, the fear of inflation is definitely back and could shake up markets further in the short-term, in case higher inflation should be confirmed and interest rates continue to rise.

Regarding China, the next data set could also give the market a new direction. Chinese stock markets have been underperforming global indices for several years, especially since pandemics. In my view, today, the glass is half full, while investors have rather a pessimistic stance, also with the threat of potential tariffs, several time announced by Trump. A lot of this is already priced in. Therefore, any positive surprise could lift stock prices in that region. At latest during the National People’s Congress in beginning of March, the government will come up with more stimulus package to support the Chinese economy.

Become a member to access more valuable market updates like this.

10.01.25 - Hot job report

As revealed by this afternoon's data, job growth in the US during December was significantly stronger than anticipated. Non-farm payrolls surged by 256’000 for the month, up from 212’000 in November and way above of the 155’000 forecasted. As a consequence, the unemployment rate came down to 4.1% (4.2% expected). The latest US job data released this afternoon came much better . The 10-year Treasury yield spiked to highest level since late 2023.

Markets: as a first reaction, interest rates and US dollar up. Stocks, cryptos, gold all down with tech and small & mid cap stocks suffering the most while energy and material sectors outperform with rising commodity prices.

My View: The year begins on a tense note, mirroring the last days on financial markets in 2024. As a consequence of rising uncertainties, investors eye on any hint by any economic release. Elevated volatility is likely to persist in the near term, keeping markets on a knife's edge until a clearer trend emerges and the pendulum begins to calm.

I continue to wait on the side-line adding more risks to my portfolio. However, I am ready for buying opportunities which could be around the corner. Better job data should actually be taken as good news regarding the overall US economy. However, investors ‘fear’ less rate cuts by the Fed than anticipated before.

Become a member to access more valuable market updates like this.

08.01.25 - All eyes on interest rates

Rumors about milder tariffs followed by Donald Trumps dementi pushed the interest rates and the inflation topic back in focus. The anticipated rate cuts by Wall Street wane. As a result, interest rates across major economies are going up, with a tilt to the longer side.

Tonight the Fed will release the minutes from its latest FOMC meeting back in December with its latest rate cut. The detailed records could provide valuable insights regarding the anticipated interest rate path in the US.

Markets: The US 10-year Treasury yield surpassed the 4.7%. With higher interest rates, more capital intense small & mid cap stocks suffer.

My View: Seems like the market wants to test the highs from October 2023 hitting the 5%.

I did not align with the prevailing consensus favoring significant rate cuts, nor do I now share investors’ heightened concerns about potential inflation. As a result, I expect interest rates to stabilize with some potential to decline. However, there is room for rates temporarily overshoot on the upside, as markets have shown a tendency to overreact recently.

It could be, that I was a slightly early adding exposure to the long-term Treasuries.

Should investors’ nervousness persist for several more days the overall sentiment could turn negative. Flight to quality kicks in. The hunt for safety and therefore US Treasuries will put yields lower again.

The last days could give a feeling what to expect during coming weeks and months. Any statement of president Trump and Elon Musk can move markets heavily in either direction as seen the last few days. An overall higher volatility level could be a reasonable consequence. Therefore the long volatility position implemented via ETF remains in my portfolio.

Become a member to access more valuable market updates like this.

07.01.25 - Fading momentum in (over)crowded trades

A notable shift in direction today in some of the most crowded trades like Palantir, Tesla, AppLovin, Nvidia etc. These stocks have been key drivers of Nasdaq’s recent rally. Today, after Nvidia set a new all-time high right after the opening bell, the positive momentum faded away and a wave of profit-taking set in as investors moved to lock in some gains.

Markets: Nasdaq Index with another significant move, dropping more than 1%. Cryptos heavily down. Interest rates are rising, faster on the longer end with the US 10-year yield close to 4.7%. European stock indices for once in the green. Gold and the US dollar gain ground with increasing uncertainties.

My View: The washout of crowded trades can be seen as both healthy and necessary, providing a reset for stocks that have experienced significant momentum. While a pause is a natural market response, the duration and severity of this pullback remain uncertain.

I took the opportunity to increase my exposure to US long-term Treasuries through an ETF, viewing it as a tactical investment move. Additionally, I took a short position on semiconductors today via an ETF, targeting a short-term investment opportunity.

I am also maintaining my short positions but have adjusted the stop limits lower to account for a potential rebound.

Become a member to access more valuable market updates like this.

06.01.25 - Hydrogen sector - strong gains

The US Department of the Treasury released today final rules for clean hydrogen production tax credit, established by the inflation reduction act. The final rules should move projects forward and help grow the industry. Companies such as Plug Power, among others, stand to benefit.

Markets: Based on the news, the hydrogen sector is among today’s top-performing industries. The sector ETF has surged almost 6%, marking a notable recovery from recent lows.

My View: Since the hype in 2021 and 2022, the sector related stocks did rather poor. Companies suffered from rising interest rates and growth fell rather short of expectations. While the sector has benefited from support under Biden’s administration, the outlook with Trump as the new president could be rather weak. However, this is already priced in since the Election Day back in November.

If the sector regains attention and builds on some positive momentum, even modest inflows could help lift these stocks from their current lows. However, volatility is likely to remain elevated, along with associated risks. I remain invested, as I believe hydrogen technology holds significant long-term potential.

Become a member to access more valuable market updates like this.

06.01.25 - Chip sector lifts market despite higher inflation data

German inflation data released today shows an uptick, back to the 3% mark. In the US, the chip market is the top gaining sector today, the day when Donald Trump is going to be confirmed by the Congress as the 47th US president.

Markets: US tech index Nasdaq again with a change above the 1% mark, this time on the upside. Chip sector in the lead, could also lift European stocks. Interest rates on the rise while cryptos show big plus.

My View: Market volume is back to be more normal as traders are back from the holiday seasons. Therefore swings could turn back to be more normal.

With the nomination of the new US president, a next wave of Trump euphoria could start as mainly risk assets are the top gainers, lead by the chip sector.

The latest inflation data in Europe highlights the already mentioned dilemma of the ECB, rising inflation with sluggish growth. Not a bullish case for European stocks.

Become a member to access more valuable market updates like this.

03.01.25 - New Year - Not a typical start

Stock indices show a bumpy ride starting the new year. Investors seem to be nervous after S&P 500 index saw worst year-end fall since 1952, losing more than 2.6% between Christmas and New Year.

Markets: US tech index Nasdaq with wide swings and volatility increase while indices in Asian and European show weakness.

My View: The last days of the year 2024 and the start of 2025 are definitely not typical compared to the usual market patterns around these days in a year.

The last days and the first days of the new year usually show some smooth moves and mostly with some gains. One of the reasons, during the first days of the years a lot of institutional money comes to market which lifts prices.

Investors are nervous after the period of pure euphoria since the Trump election and elevated price levels.

It will be interesting to follow the moves beginning of next week when everyone is back from the holiday season.

Become a member to access more valuable market updates like this.

27.12.24 - Hefty swings amid low volumes

The holiday season brings thin trading, and the Nasdaq is swinging wildly - 1% moves up or down - despite low volumes.

Markets: US tech stock index Nasdaq is currently down more down 2% intraday. The index has been experiencing significant fluctuations, with moves exceeding 1% in both directions during recent trading sessions.

My View: Today’s 2% drop underscores how small trades can amplify volatility in a quiet market. These moves stem rather from technical dynamics, not fundamentals, as reduced liquidity leaves the market vulnerable to outsized reactions. As outlined the days before, investors should be a bit more cautious; these swings are seasonal quirks, not opportunities. For now, it’s wise to watch from the sidelines, not adding more risk to the portfolio and focus on the new year ahead.

Become a member to access more valuable market updates like this.

23.12.24 - Markets stabilized

After the latest US inflation print on Friday afternoon and as the US government shutdown was averted, investors started to calm down.

Markets: Steady trading day with subdued volumes ahead of the holiday-related stock market closures across markets.

My View: Positive sign that markets could stabilize before the holiday season starts with low volumes.

Inflation and economic data will remain in focus in the beginning of 2025. Any negative surprise could lead to a sharp market reaction. Furthermore, the focus will be on Trump and his first days as the US president which could also have the potential and lead to market swings in either direction.

Become a member to access more valuable market updates like this.

20.12.24 - Sell-off continues

After the latest US inflation print on Friday afternoon and as the US government shutdown was averted, investors started to calm down.

Markets: Steady trading day with subdued volumes ahead of the holiday-related stock market closures across markets.

My View: Positive sign that markets could stabilize before the holiday season starts with low volumes.

Inflation and economic data will remain in focus in the beginning of 2025. Any negative surprise could lead to a sharp market reaction. Furthermore, the focus will be on Trump and his first days as the US president which could also have the potential and lead to market swings in either direction.

Become a member to access more valuable market updates like this.

19.12.24 - Stock market sell-off

Global stock market tumble following the US stock markets lower after the Fed release yesterday. The US central bank cut the key rate by 0.25% as expected. However, the Fed is likely to cut interest rates less than previously anticipated in 2025 as inflation persists.

Markets: US Dow Jones Industrial Average closed over 1’100 points lower adding to the streak of 10 consecutive days with losses, the worst since 1974. Nasdaq was down almost 4% while interest rates ended higher with the 10-year Treasury yield above 4.5% again. Asian and European stock markets followed the US currently trading down. Commodities, gold and silver tanked as well while volatility soared.

My view: as highlighted already during the last days, the potential for a correction is around the corner as too much of optimism was priced in. Therefore, this sharp move lower of US stocks does not come as a surprise to me as well as the spill-over on global stock markets, gold and silver, mentioned as well.

The good news about, the US economy is doing well as the speed of the rate cut cycle can be lowered.

I keep the wait and see stance if the euphoric buyers and optimists are coming back to the market right away or the correction has some potential to continue. Right now the US markets is set for a small rebound. Let’s see if this rebound is only of technical nature or attracts more buyers again.

Become a member to access more valuable market updates like this.

18.12.24 - Worst streak in 46 years

Investors are somewhat puzzled by the 9 straight days of losses. While US equities churn near all-time highs, one of the closely watched indexes in the US shows its worst losing streak since 1978. The Dow Jones Industrial Average has fallen for 9 consecutive days.

Markets: US Dow Jones Industrial Average closed lower for 9 straight days while Nasdaq climbs to new record highs.

My view: Nothing to panic yet. The Dow is a stock price-weighted index. The shares of UnitedHealth have been primarily dragging the index down. While notable gainers including the tech members Microsoft, Apple and Amazone were not able to absorb the negative impact.

I do not see this as a buying opportunity. As mentioned before, US tech stocks show an overbought level with the pure optimism. Such kind of news could suddenly change investors’ sentiment and lead to some profit taking.

Become a member to access more valuable market updates like this.

17.12.24 - All-in - record low cash levels reported

All-in stance on US equities. The latest survey of fund managers released by Bank of America shows record low levels of cash. Investors push US equity indices to record highs on pure optimisms since US presidential election and the Trump victory.

Markets: US equity indices reach new record highs almost on a daily basis.

My view: the skyrocketing tech stocks combined with the low cash level I rather take as a contrarian indicator. Stocks correction can be around the corner any time soon. However, the momentum can still last for more days. A fact to keep in mind, that during the holiday season, the market liquidity is going to be on a reduced level. Therefore, bigger moves in either direction could be expected.

After the big run of US equities, reducing some positions to rise some cash could be of advantage. At the same time I added some short positions with some lately skyrocketing stocks like Palantir, AppLovin, Netflix, Arista Network, and latest addition Tesla, while I keep the short on Nvidia. Furthermore, I expect an increase in volatility. To benefit and for some hedging purpose I added an ETF on long volatility.

Become a member to access more valuable market updates like this.

16.12.24 - All eyes on the Fed release

Investors eye on the release of the US Federal reserve (Fed) policy decision on coming Wednesday evening. A interest rate cut of 0.25% is widely anticipated.

Markets: Investors and markets are rather calm and in awaiting stance. Asian and European equity markets are trading sideways in negative territory while US futures, mainly tech, are gaining ground by optimistic investors. Same picture on the currency front and for interest rates, trading sideways in a narrow stance.

My view: A rate cut by the Fed is already priced in. The primary focus will be on policymakers' outlook for next year depending on the economic growth and persistent inflation. Currently, the market prices in a moderate interest cut cycle for 2025. Any disappointment in the communication on the pace of rate cuts could lead to a profit taking stance in elevated US equity markets, especially in tech stocks. USD, gold and silver would also be affected while US interest rates would decline. Global markets may then be dragged down as well.

Become a member to access more valuable market updates like this.

12.12.24 - Rate cut cycle continues

The European Central Bank (ECB) cuts the key rate by 0.25% (as expected) to 3%.

Markets: Euro continue to weaken against the USD. No impact on equity side.

My view: As I wrote already in my blog article “Europe, the struggling candidate – time for the pole-position, finally?” (15.07.2024), the European economy remains fragile due to several reasons. Furthermore, the ECB remains in an unfavorable position. On one hand, to fight against inflation which remains elevated in the European region. On the other hand, being less restrictive in its monetary policy to support the struggling economic environment. Therefore my view remains unchanged - no big potential for European equity indices in the mid-term, however, selectively remain invested.

Become a member to access more valuable market updates like this.

12.12.24 - SNB surprises markets

Swiss National Bank (SNB) cuts key interest rate by 50bps, analysts consensus expected 25bps.

Markets: Swiss franc (CHF) weakens against major peers. Swiss equity indices see a smaller gains after the announcement.

My view: Even SNB surprises with the bigger than expected rate cut, I see the market impact rather short-lived. The currently priced-in expectations of negative interest rates in 2025 seem exaggerated. Therefore Swiss equities might continue to lag as other regions remain more in focus. Currency wise, the Swiss Franc will not lose much more ground from here as other central banks remain in the rate cut cycle too, as ECB at noon today.

Become a member to access more valuable market updates like this.